The Decline of Pandemic Savings: Economic Implications

-

Jan, Sat, 2025

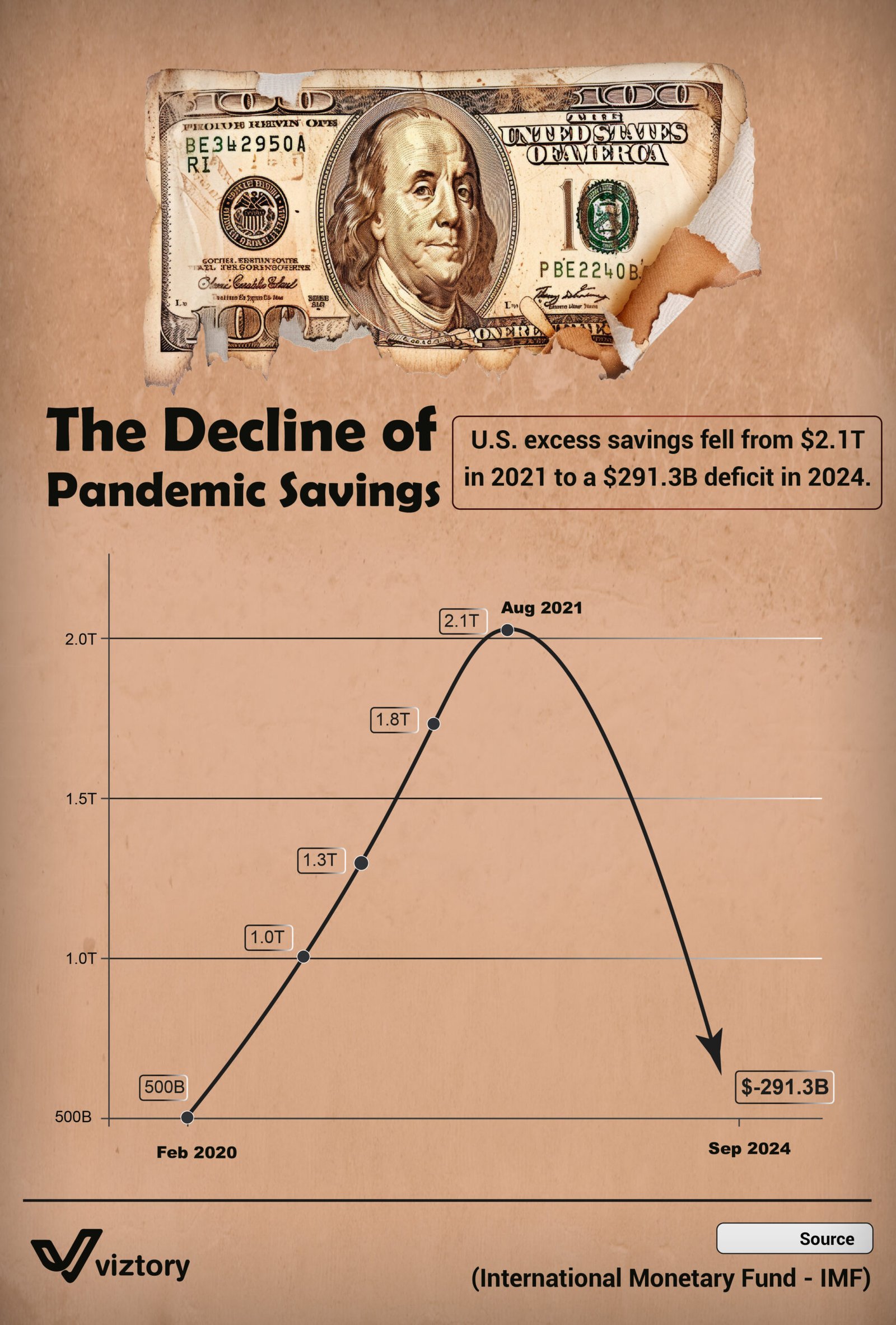

The COVID-19 pandemic reshaped global financial behaviors, with households in the United States amassing unprecedented levels of savings due to reduced spending and government stimulus packages. However, as this visualization highlights, U.S. excess savings have dwindled dramatically, falling from a peak of $2.1 trillion in August 2021 to a deficit of $291.3 billion by September 2024. This trend raises critical questions about the economic landscape and consumer resilience in the face of financial pressures.

The Journey of Pandemic Savings

Early Pandemic Period (Feb 2020)

- Savings began at $500 billion, fueled by precautionary behavior and reduced discretionary spending during lockdowns.

- Economic Impact: Government relief packages contributed to initial savings growth.

Rapid Accumulation (2020–2021)

- Savings peaked at $2.1 trillion in August 2021 due to stimulus checks, expanded unemployment benefits, and low consumer spending.

- Economic Impact: These savings temporarily boosted the economy through delayed spending on goods and services.

Decline Begins (2022)

- As inflation rose and pandemic-related aid ended, households began drawing on their savings to meet rising costs.

- Economic Impact: Consumer spending helped sustain economic recovery but depleted savings reserves.

Sharp Drop (2023–2024)

- By September 2024, savings turned into a deficit of $291.3 billion, indicating households are spending beyond their income.

- Economic Impact: Rising debt and reduced disposable income pose challenges for long-term economic growth.

Key Economic Factors Driving the Decline

Inflation

- Persistent inflation since 2022 has eroded purchasing power, forcing households to dip into savings for essential expenses.

Rising Interest Rates

- Central banks, including the Federal Reserve, raised interest rates to combat inflation, increasing borrowing costs for households and businesses.

Post-Stimulus Economic Adjustment

- The end of government aid programs left many households unprepared for the financial pressures of a “normal” economy.

Shifts in Consumer Behavior

- Pent-up demand for travel, dining, and other discretionary spending surged as pandemic restrictions eased, accelerating savings depletion.

Broader Economic Implications

Consumer Spending and Growth

- With savings depleted, consumer spending—a major driver of the U.S. economy—may slow, impacting GDP growth.

Household Debt

- The shift from savings to deficit suggests increased reliance on credit, leading to higher levels of household debt.

Financial Vulnerability

- Low savings leave households less prepared for economic shocks, such as job losses or unexpected expenses.

Policy Considerations

- Policymakers may need to consider targeted measures to support struggling households, such as tax relief or subsidies for essential goods.

Strategies for Economic Resilience

Encouraging Financial Literacy

- Promoting saving and budgeting habits can help households rebuild financial cushions.

Targeted Stimulus

- Future economic relief efforts could focus on lower-income households disproportionately affected by inflation and rising costs.

Inflation Control

- Continued efforts by central banks to manage inflation are critical for restoring financial stability.

This steep decline in pandemic savings serves as a stark reminder of how quickly economic conditions can shift. It underscores the importance of balancing short-term relief with long-term financial resilience for households and the broader economy.